The Ministry of Finance has issued Regulation No. 8 of 2026 (“PMK 8”), which amends PMK228/PMK.03/2017 (“PMK-228”) regarding Details of Types of Data and Information and Procedures for the Submission of Data and Information Related to Taxation.

OVERVIEW OF THE CHANGES

Similar to PMK-228, PMK 8 aims to provide legal certainty and establish clearer procedures for the submission of data by government agencies, institutions, associations, and other relevant parties to the Director General of Taxes (the DGT). However, PMK 8 further refines these provisions by:

✓ Clarifying procedures for both the submission and utilization of data; and

✓ Introducing more explicit mechanisms to be followed where the DGT considers that the submitted data is insufficient.

A notable enhancement under PMK 8 is the expansion of the list of government agencies and institutions required to provide data, as set out in its attachments

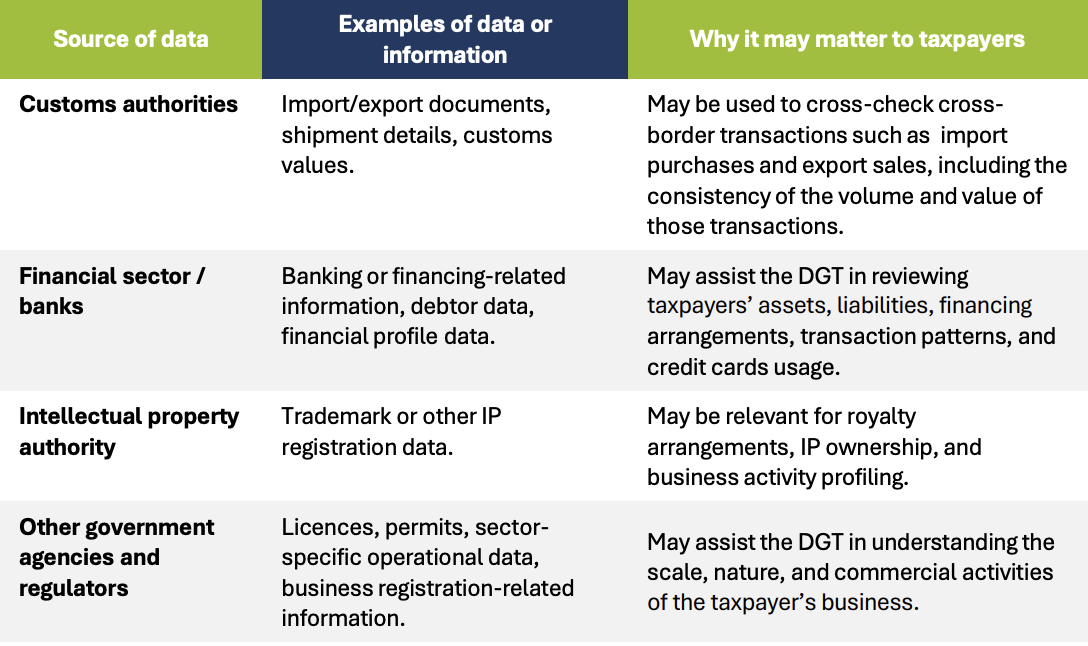

- the Directorate General of Economic and Fiscal Strategy (Direktorat Jenderal Strategi Ekonomi dan Fiskal);

- the Directorate General of Intellectual Property (Direktorat Jenderal Kekayaan Intelektual);

- the Financial Services Authority (Otoritas Jasa Keuangan);

- the Downstream Oil and Gas Regulatory Agency (BPH Migas);

- the IndonesianQuarantine Agency (Badan Karantina Indonesia);

- the Ministry of Hajj and Umrah (Kementerian Haji dan Umrah); and

- the State-Owned Enterprises Regulatory Agency (Badan Pengaturan BUMN).

WHAT THIS MEANS IN PRACTICE

Notwithstanding the above, the use of third-party data is not entirely new. Taxpayers familiar with the SP2DK process will recognize that the DGT has long relied on data from various institutions to verify and confirm taxpayer positions. In practice, this may include, for example, customs data, banking or financial information, and other third-party records. Accordingly, PMK 8 can be viewed as formalizing, expanding, and updating the DGT’s legal basis and institutional access to such data.

The inclusion of additional institutions suggest that the range of data available to the DGT may become broader and more varied going forward. In particular with the data from Otoritas Jasa Keuangan (“OJK”) as government agency that regulating and supervising financial services activities in the banking sector, capital markets, and non-bank financial services sectors (such as insurance, pension funds, etc.), the DGT may now easily check and identify inconsistency between the data reported in the taxpayers’ tax return and the financial data obtained by OJK such as income from investment, assets, liabilities, credit facility, etc.

Challenges may arise where discrepancies arise between different data sources, requiring taxpayers to substantiate and reconcile their positions with adequate explanations and supporting documentation. Examples of third-party data that may be relevant to taxpayers

Examples of third-party data that may be relevant to taxpayers

KEY TAKEAWAYS

For taxpayers, data consistency will become increasingly critical. As the DGT gains broader access to third-party data and operating within a more integrated, data-driven compliance framework, discrepancies are more likely to be identified at an earlier stage.

Taxpayers should therefore ensure that tax filings are aligned with information reported to other government agencies and institutions, particularly in key areas such as:

- imports and export transaction, based on data from the customs authority’s system;

- financing arrangement and financial position (e.g. loans, credit facilities);

- assets and investment income; and

- other operational and business activities.

Proactive reconciliation and robust supporting documentation will be essential to mitigate the risk of queries or challenges arising from inconsistencies across data sources.