On 30 December 2025, the Ministry of Finance issued Regulation Number 112 of 2025 (PMK-112) regarding the Procedures for the Implementation of the Tax Treaty. The regulation serves as the implementing guideline for Article 50(2) of Government Regulation No. 55 of 2022, specifically concerning the Application of Double Taxation Avoidance Agreements or Tax Treaty.

PMK-112 incorporates the procedures for Resident Taxpayers (“WPDN”) and Non-Resident Taxpayers (“WPLN”) in claiming Tax Treaty benefits that were previously regulated separately under Director General of Taxes (DGT) RegulationNo. PER-28/PJ/2018 (PER-28) and PER-25/PJ/2018 (PER-25), respectively.

PMK-112 structured into three (3) primary sections.

- Procedure for WPLN: Outlining how Indonesian residents claim treaty benefits abroad;

- Procedure for WPDN: Detailing how WPLN claim treaty benefits on Indonesian-sourced income; and

- Prevention of Tax Treaty Abuse: Introducing anti-avoidance measures for certain events or transactions.

The procedures set out in PMK-112 are largely similar to those stipulated in PER-28 and PER-25, with certain updates to the requirements and administrative procedures for claiming Tax Treaty benefits.

This Tax Highlights addresses only the procedures for the implementation of Tax Treaty for WPLN and the prevention of Tax Treaty abuse.

1. PROCEDURES OF APPLYING THE TAX TREATY FOR WPLN

WPLN is entitled to obtain the Tax Treaty benefits, provided that such Non-Resident Taxpayer:

- is not an Indonesian Domestic Tax Subject;

- is a resident of a Tax Treaty Partner Country for tax purposes; and

- does not engage in any abuse or misuse of the Tax Treaty.

The previous requirement in PER-25 that the income recipient must be the beneficial owner has been removed as a standalone condition. However, this requirement is incorporated as one of the criteria in determining the existence of Tax Treaty abuse under PMK-112.

Requirements of the Directorate General of Taxes Form

WPLN who receive or derive income sourced from Indonesia must provide a Certificate of Domicile or the Directorate General of Taxes form (DGT Form) to apply treaty benefits. DGT Form must meet the following administrative requirements:

a. must be completed correctly, completely, and clearly;

b. must be signed (or marked by an equivalent of signature) by the WPLN;

c. must be validated by being signed (or marked with an equivalent of signature) by the Competent Authority of the treaty partner country.

d. used for the period stated in the DGT Form; and

e. prepared using the new format as stated in PMK-112 Attachment.

Consistent with requirements above, the DGT Form is also streamlined into 6 parts (down from 7) by consolidating the anti-abuse and the Beneficial Ownership (BO) test requirement, into Part V. With this change, the BO requirement must be completed for any Indonesian-sourced income received by WPLN, and are no longer limited only to dividend, interest and royalty. All the requirements remain largely the same as the previous DGT Form.

Other updates are as follows:

❑ WPLN may use a Certificate of Domicile (“CoD”) issued by the competent authority of treaty partner as a replacement for the legalization of the DGT Form as long as it fulfills the requirements. If the CoD does not mention a validity period, it should be valid for the month in which it is issued,

❑ Upon receiving the DGT Form, the Indonesian withholder is required to verify the taxpayer’s entitlement to claim thr Tax Treaty benefits and compliance with the applicable formal requirements, based on the relevant accounting records and supporting documents as the basis for withholding tax (“WHT”) purposes.

-

- If the requirements are met: The withholder must upload the DGT Form via the Coretax portal, receive the DGT Form receipt, submit the DGT Form Receipt to WPLN and withhold WHT based on the relevant Tax Treaty.

- If the requirements are not met: The withholder must apply the domestic Income Tax rate (typically 20% under Art. 26 of Income Tax Law).

❑ A WPLN that has obtained the DGT Form receipt may re-use the same DGT Form for subsequent income by the same or another Indonesian withholder within its validity period without resubmitting the form. However, each subsequent withholder remains obligated to independently verify compliance based on the available supporting documents.

The DGT Form in Audit and Compliance

For audit purpose, the Indonesian withholder shall keep the following documents in accordance with Law on General Provisions and Tax Procedures:

- The DGT Form and the receipt,

- CoD if the DGT Form is unavailable, and

- The books of account, records and/or documents that serve as proof of the underlying transactions.

PMK-112 emphasizes that if the DGT Form submitted to the DGT during tax audit, objection, and during the process of a request for reduction/cancellation of tax assessment letter, such DGT Form may still be considered as a basis for tax imposition in accordance with the relevant Tax Treaty.

Please note however, the acceptance may depend on the DGT’s discretion. To mitigate this risk, the Indonesian withholder should consistently submit the DGT Form in timely manner and report the DGT Form receipt together with the monthly WHT Returns.

2. PREVENTION OF TAX TREATY ABUSE

Under PMK-112, the Tax Treaty abuse refers to any attempt by a WPLN to reduce, avoid, or defer income tax in a way that contradicts the purpose and objectives of the Tax Treaty. PMK-112 further clarifies the purpose and objective of the Tax Treaty are to eliminate double taxation while preventing non-taxation or reduced taxation arising from tax avoidance or evasion, including treaty shopping by third-country residents. This clarification is in accordance with Article 6 of the OECD Multilateral Instrument (“MLI”) on preventing treaty abuse as well as the preamble of the current OECD Model Convention.

The DGT may conduct a compliance test in accordance with the provisions of the applicable Tax Treaty or, where the treaty does not contain specific compliance provisions, apply the anti-abuse rules under the Income Tax Law. Where the compliance test indicates that the relevant requirements are not satisfied, the taxpayer’s tax liabilities will be determined in accordance with the Income Tax Law.

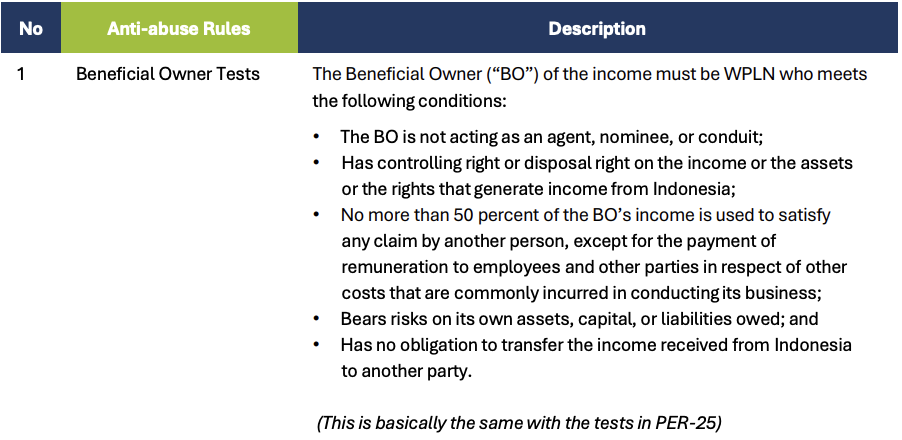

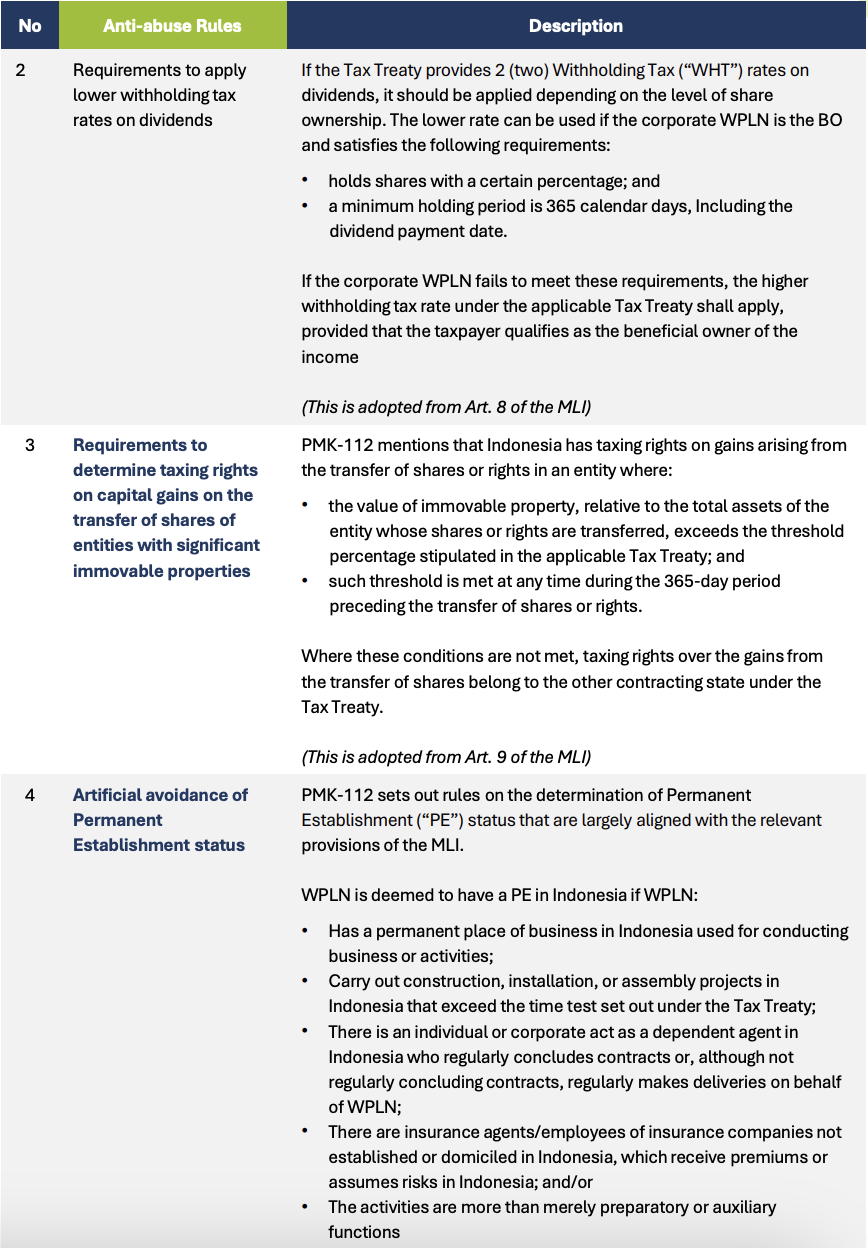

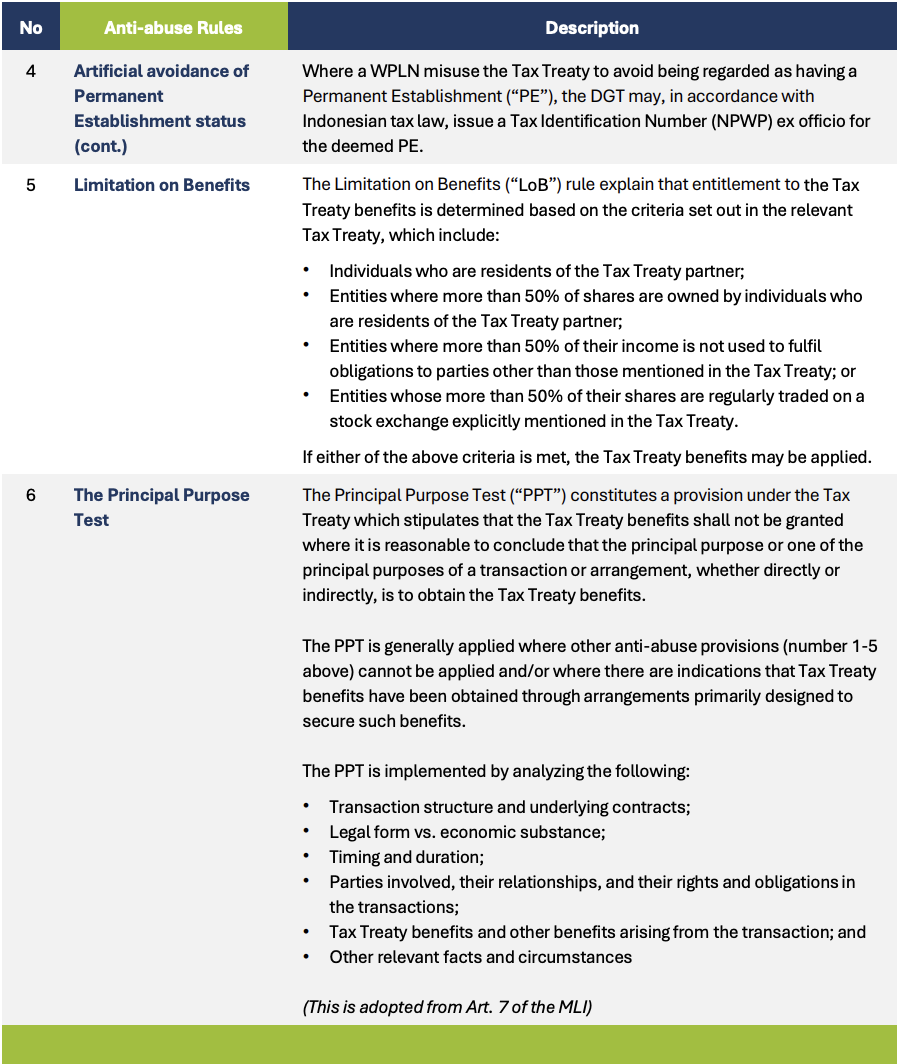

The anti-abuse rules

PMK-112 adopts several anti-abuse rules from the MLI, which are applied as compliance tests in determining a taxpayer’s eligibility to obtain Tax Treaty benefits. The applicable anti-abuse rules under PMK-112 are summarized in the table below.

PMK-112 does not expressly state that these rules apply only where they are incorporated into the relevant Tax Treaty. However, the illustrative examples set out in the Appendix indicate that their application is intended for situations in which such rules have been adopted in the relevant Tax Treaty.

3. TRANSITIONAL PROVISIONS

PMK-112 officially took effect on 31 December 2025. PMK-112 does not provide transitional provision. Based on the Announcement number PENG-2/PJ.09/2026 released by the DGT, the DGT Forms obtained before 30 December 2025 may continue to be used until their original expiry date. Once the old form expires, or for any new transactions initiated after the effective date of PMK-112, the new DGT Form format must be used.