The Ministry of Finance has issued Regulation No. 111 of 2025 (“PMK-111”) regarding Taxpayer Compliance Supervision (“Pengawasan Kepatuhan Wajib Pajak”). The regulation is issued to provide guidance to taxpayers in relation to the implementation of the tax self-assessment system, which is necessary to conduct supervision over taxpayers’ fulfillment of their tax obligations. It also aims to ensure the supervision process is fairer and provides greater legal certainty by establishing clear rules on how supervision is conducted.

PMK-111 is effective from 1 January 2026.

Under PMK-111, “Supervision” is broadly defined as a series of verification activities on a taxpayer’s fulfillment of tax obligations, whether obligations that will be performed, have not been performed, or have been performed, with the objective of promoting compliance with the prevailing tax laws and regulations.

1. SCOPE OF SUPERVISION

PMK-111 stipulates that there are three (3) categories of Supervision, as follows:

a. Supervision of registered taxpayers;

b. Supervision of unregistered taxpayers; and

c. Regional supervision.

Supervision is conducted based on the Directorate General of Taxes (“DGT”) verification of data and/or information available to the tax authority. The scope covers various taxes administered by the DGT, including but not limited to Income Tax, VAT, Luxury Goods Sales Tax, Stamp Duty, Land & Building Tax (for certain sectors), Carbon Tax, and other taxes under the DGT’s authority.

PMK-111 also clarifies the compliance aspects that may be supervised, including (among others) Tax Returns (Surat Pemberitahuan or SPT) filing, tax payment/settlement, withholding obligations, bookkeeping/recordkeeping, VATable Entreprenuer (PKP) obligations, and reporting of business locations (“NITKU”).

This Tax Highlight focuses only on information relating to the supervision of registered taxpayers and does not address other forms of supervision.

2. REGISTERED TAXPAYERS’ SUPERVISION ACTIVITIES

PMK-111 sets out the forms of supervision activities that may be carried out by the DGT on registered taxpayers, including:

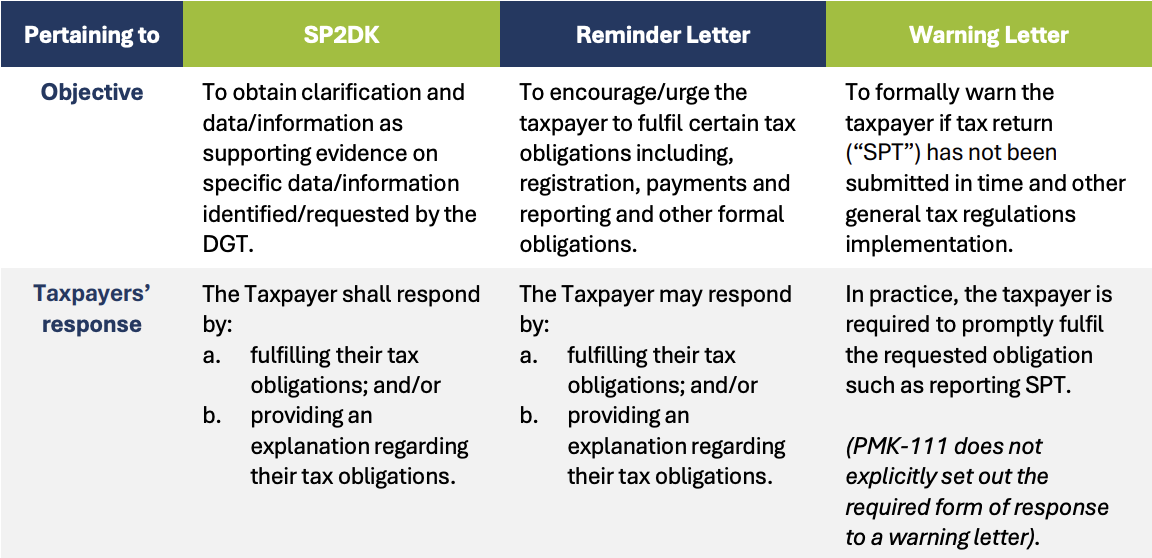

a. Requesting explanation on certain data and/or information from the taxpayer (Surat Permintaan Penjelasan atas Data dan/atau Keterangan or SP2DK);

b. Conducting discussion with the taxpayer;

c. Inviting the taxpayer to attend a meeting (offline or online);

d. Visiting the taxpayer;

e. Issuing a reminder letter (surat imbauan);

f. Issuing a warning letter (surat teguran);

g. Requesting transfer pricing documentation;

h. Collecting regional economic data;

i. Issuing letters for supervision purposes; and

j. Performing other supporting supervision activities.

The following section discusses an overview of SP2DK, the reminder letter, and the warning letter, as these are stipulated under PMK-111, which are among the commonly issued supervision instruments by the Directorate General of Taxes (DGT) to taxpayers.

3. KEY PROCESSES AND TIMELINES

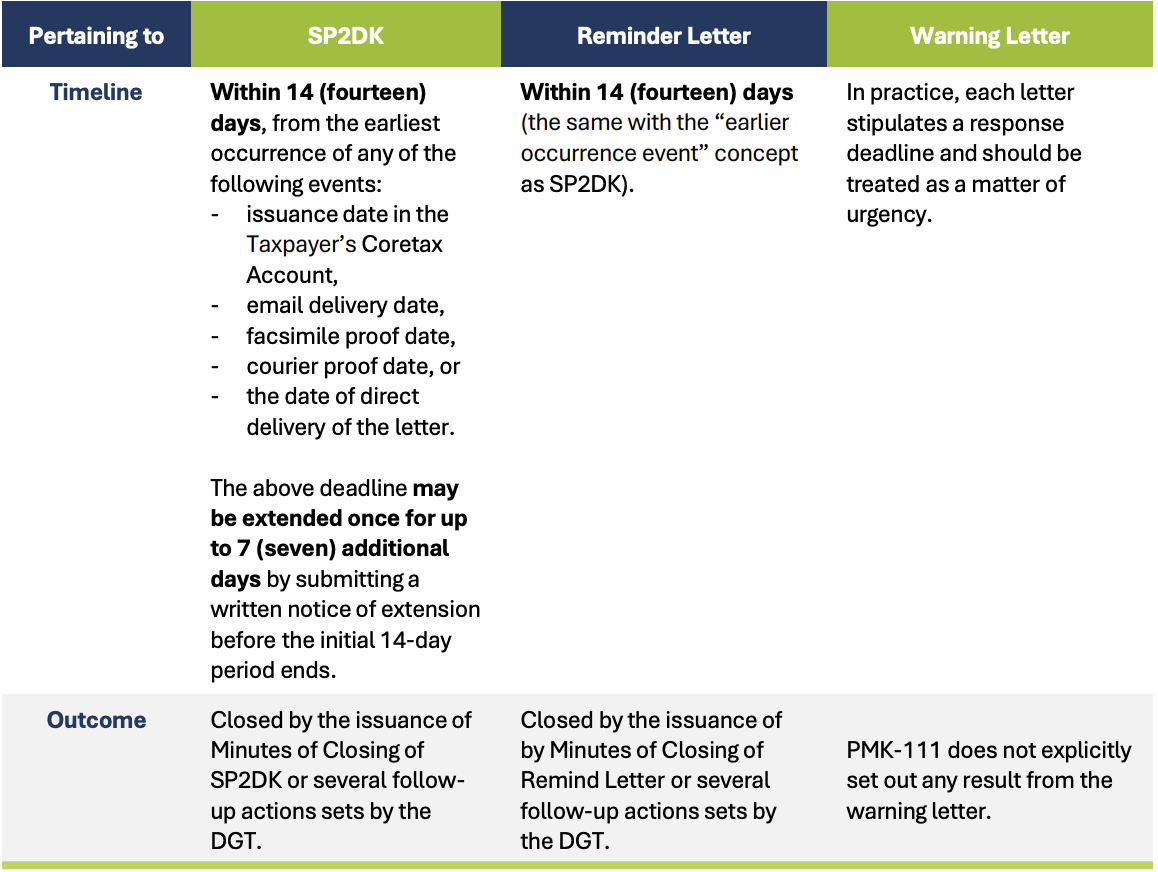

The table below sets out a comparative overview of SP2DK, reminder letters, and warning letters, highlighting the applicable response deadlines and the possible subsequent actions by the DGT that taxpayers should anticipate.

The above letters (SP2DK, reminder letter, and warning letter) are issued by the DGT and should be responded by the taxpayer through the following actions.

– Taxpayer’s Coretax Account,

– post/courier service,

– direct submission during the DGT’s visit

– direct submission to the registered Tax Office/ via video conference (for a response to the SP2DK and reminder letter)

If based on the DGT’s verification, the Taxpayer’s response is in accordance with the request stated in SP2DK, the DGT will prepare an official minutes/report on the implementation of SP2DK.

Further follow-up may be conducted where:

– the taxpayer’s response is not in accordance with the request outlined in SP2DK,

– there is an additional data and/or information obtained after SP2DK is delivered, or,

– the taxpayer does not provide a response within the timeline (including any extension period stated in SP2DK).

In such cases, the DGT may proceed with a discussion by inviting the taxpayer to a meeting or by conducting a visit. These discussions may take place either in person or via video conference. Upon completion of the discussion, the DGT will issue Minutes of Meeting (Berita Acara Pembahasan SP2DK) as an official record of the SP2DK process. In certain circumstances, the DGT may request a further follow-up discussion by issuing a new invitation.

In principle, the procedures for handling the reminder letter follow the similar process.

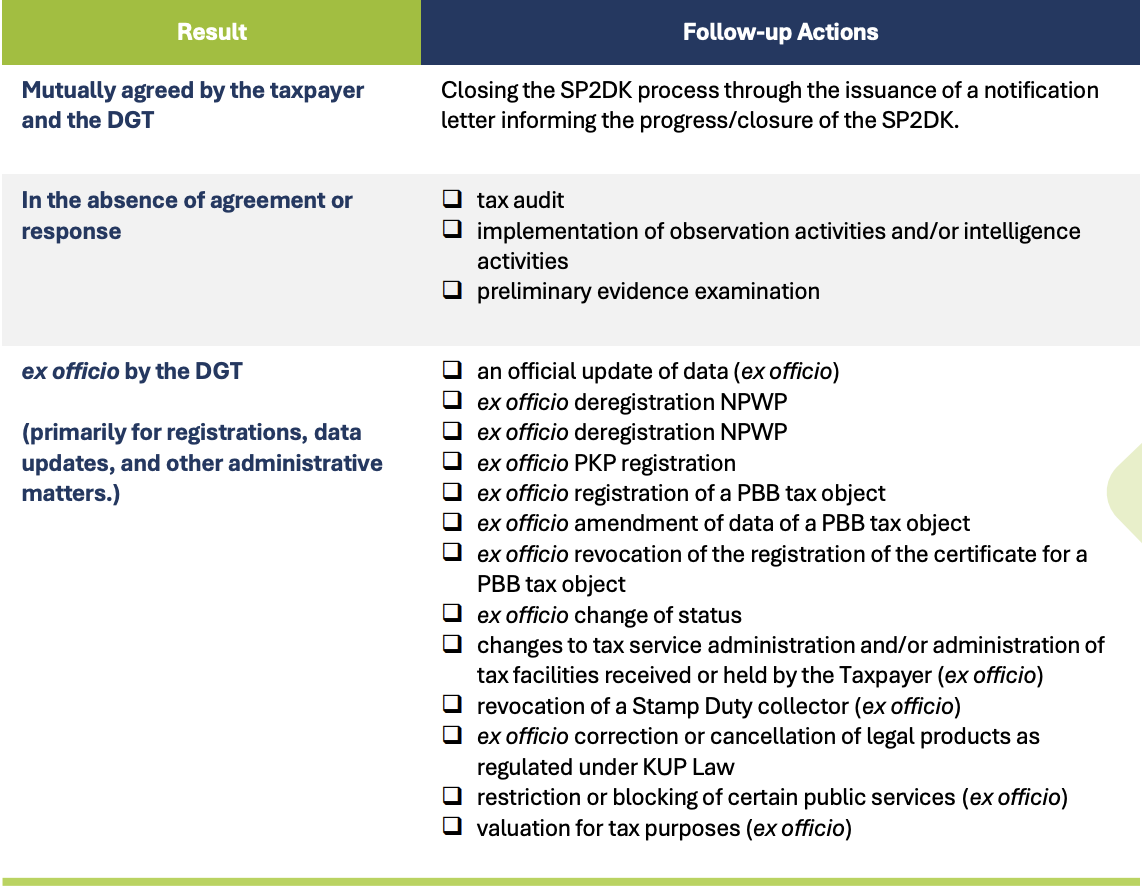

4. POTENTIAL OUTCOMES FOLLOWING SP2DK

Unlike reminder letters and warning letters, which primarily relate to the fulfilment of tax obligations and administrative compliance, an SP2DK may lead to further follow-up actions by the DGT.

Art. 8 of PMK-111 sets out 17 (seventeen) possible follow-up actions that may be carried out by the DGT:

5. PRACTICAL IMPLICATIONS FOR TAXPAYERS

❑ Tight response timeline for SP2DK

Taxpayers should establish internal SOPs to ensure SP2DK responses can be submitted within 14 days, including an early assessment of whether a one-time 7-day extension is necessary. All relevant reconciliations should be properly prepared in advance, as insufficient data preparation may result in the statutory deadline not being met.

❑ Coretax readiness

As the delivery of notices and the commencement of the response timeline may be linked to the taxpayer’s Coretax account, taxpayers should ensure that the account remains accessible at all time and that responsible PICs are assigned to monitor incoming correspondence and coordinate timely responses to DGT.

❑ Transfer Pricing Documentation readiness

Transfer Pricing documentation (Dokumen Lokal) should be prepared in accordance with the prescribed timeline regardless of whether the taxpayer is under a tax audit. The DGT may request Dokumen Lokal during the supervision phase in the context of SP2DK. Therefore, taxpayers should ensure that Dokumen Lokal is readily available and aligned with the arm’s length principle and the documentation requirements under PMK-172/2023, without waiting for a formal tax audit to commence.

❑ Clear escalation path

PMK-111 confirms that Supervision may progress from clarification stage to discussion/visit which may lead to various outcomes (including tax audit and preliminary evidence examination), depending on the circumstances and findings.

PMK-111 emphasizes that SP2DK, Reminder Letter and Warning letter must be properly responded to avoid unnecessary issues or follow-up actions by the DGT. In particular, SP2DK should be treated with due care, as the taxpayer is expected to demonstrate — through a clear explanation supported by adequate documentation — that their tax obligations have been fulfilled in accordance with the prevailing tax laws and regulations.