To ensure legal protection and certainty, as well as ease employees and the public in submitting complaints regarding alleged misconduct within the Directorate General of Taxes (“DGT”), the DGT has issued Regulation No. 21/2025 (“PER-21”). This regulation aims to prevent the following types of misconduct:

- The provision of tax services by the DGT that does not comply with the established

service standards, prevailing laws and regulations, - Tax-related criminal acts, and;

- Violations of the code of ethics, code of conduct, and employee discipline within the

DGT.

PER-21 is intended to establish effective, efficient, transparent and accountable procedures for the submission of complaints against alleged misconduct within the DGT.

PER-21 only regulates the administrative procedures for the submission of complaints to the DGT and does not provide detailed definitions or classifications of reportable misconduct. Accordingly, the determination of whether a particular act constitutes reportable misconduct, should be made by reference to the relevant underlying regulations (e.g., ethics-related matters should be assessed under Minister of Finance Regulation No. 190/PMK.01/2018 regarding the Code of Ethics and Code of Conduct for Civil Servants within the Ministry of Finance).

From a taxpayer’s perspective, questions may remain as to how practical this regulation can be utilized to submit complaints arising from dissatisfaction with tax services. In practice, the category that appears most relevant and readily applicable to taxpayers is complaints concerning non-compliance with tax service standards, while the other categories may be less relevant or less frequently used by taxpayers in general. Ultimately, the effectiveness of this regulation will depend on how it is implemented in practice.

PER-21 is effective on 28 November 2025.

1. MINIMUM INFORMATION REQUIRED

In submitting a complaint in respect of any of the three types of misconduct above, the minimum required information is generally the same, as summarized below.

- Identity of the complainant

- Contact details (telephone or email)

- Identity of the reported party

- Explanation regarding the complaint (alleged misconduct)

- Date and location of the incident (if applicable)

- Supporting documents or evidence (if available)

Please refer to Art. 4, Art. 7, and Art 9 PER-21 for more details on the matter. In addition, it should be noted that anonymous complaints for tax-related criminal act may be processed, provided they are supported by sufficient and credible evidence.

2. COMPLAINT HANDLING AND TIMELINE

PER-21 sets out the procedures and timelines for the DGT in handling complaints. For instance, the procedures for processing complaints regarding tax services can be summarized as follows:

- A complaint regarding tax services must be submitted within 30 days from the date of the incident.

- The DGT will conduct an initial review to assess the completeness of the complaint.

- Complaint that is deemed complete will be processed within 30 business days from the receipt date.

- If the complaint is deemed incomplete, the DGT will request additional information.

- The complainant must provide the requested information within 14 business days.

- If the requested information is not provided within the prescribed timeframe, the complaint may not be processed further.

For complaints regarding tax-related criminal acts and violations of the code of ethics, code of conduct, and employee discipline within the DGT, PER-21 does not prescribe a deadline for the submission of such complaints. However, the handling of tax crime complaints is subject to a shorter response timeline, requiring the relevant unit to undertake follow-up action within five (5) business days.

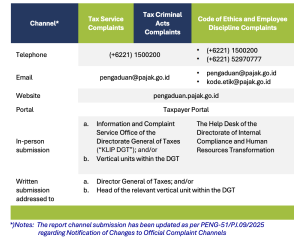

3. SUBMISSION CHANNEL FOR THE COMPLAINTS

Complaint applications must be submitted through the official channels of the DGT which include:

The DGT has provided a standard complaint submission template in the appendix of PER21 which can be used for all types of complaints.

B. UPDATE ON TAX BILLING IN CORETAX: EXTENDED VALIDITY AND CANCELLATION FEATURE

1. Extension of Tax Billing Code Validity Period

The Directorate General of Taxes (“DGT”) has issued Announcement No. PENG-4/PJ/2025, which introduces an update extending the validity period of tax billing codes (kode billing) in order to support taxpayers in fulfilling its tax obligations. Under DGT Regulation No. PER-10/PJ/2024, a billing code is generally valid for 168 hours (7 × 24 hours) from the date of issuance. In practice, however, taxpayers may face circumstances beyond their control (force majeure) that prevent timely tax payment, such as network disruptions, administrative complexities involving third parties, cross-border payment procedures through international correspondent banks, or consecutive national holidays and collective leave.

To address these practical challenges and to prevent failed tax payments due to expired billing codes, the DGT introduce a new policy:

- the validity period of billing codes is extended to 336 hours (14 × 24 hours) from the time the billing code is issued.

- the extended validity period applies to billing codes generated from the issuance date of the announcement onward.

However, billing codes in the Coretax system can only be generated after taxpayers have completed the preparation of the relevant tax return. Therefore, the extension of billing codes is unlikely to have a significantly impact on day-to-day tax compliance and filing activities.

2. Cancellation of Tax Billing Code

Effective per 1 December 2025, Coretax introduces a new feature that allows taxpayers to cancel an unpaid tax billing code generated from a draft Tax Return (SPT). Once cancelled, the system will revert the SPT status from “Waiting for Payment” (Menunggu Pembayaran) back to “Draft” (Konsep).

This update is intended to provide convenience for taxpayers, as it allows taxpayers to revise the draft of tax returns and generate a new billing code without having to wait for the previous billing code to expire. Previously, taxpayers generally had to wait for the expiration of the existing billing code before revising the tax return. As such, this enhancement facilitates a more practical and efficient tax compliance process.